i-80 Gold Reports Q3 2022 Operating Results

Reno, Nevada, November 8, 2022 – i-80 GOLD CORP. (TSX:IAU) (NYSE:IAUX) (“i-80”, or the “Company”) is pleased to report its operating and financial results for the three and nine months ended September 30, 2022. i-80’s Consolidated Financial Statements (“financial statements”), as well as i-80’s Management’s Discussion and Analysis of Operations and Financial Condition (“MD&A”) for the three and nine months ended September 30, 2022, are available on the Company’s website at www.i80gold.com, on SEDAR at www.sedar.com, and on EDGAR at www.sec.gov.

Unless otherwise stated, all amounts referred to herein are in U.S. dollars.

2022 Third Quarter Highlights:

-

- Record quarterly gold sales of 9,332 ounces; all-in sustaining cost of $1,138 per ounce sold1

- September 30 cash balance of $76 million and $33 million in restricted cash

- Drilling at Granite Creek continued with multiple high-grade intercepts in the Ogee and South Pacific zones (10,526 core feet and 5,460 reverse circulation (RC) feet drilled)

- First shipment of sulfide mineralized material from Granite Creek was made to NGM’s Twin Creeks processing facility

- Continued step-out and infill drilling at Ruby Hill with multiple high-grade intercepts and new discoveries made (17,025 core feet and 34,865 RC feet drilled)

- Engineering study of Lone Tree autoclave refurbishment continued on plan

2022 Year to date Highlights:

-

- Gold sales of 14,328 ounces; all-in sustaining cost of $1,204 per ounce sold1

- Commenced trading on the New York Stock Exchange on May 19, 2022 under the symbol IAUX

- Funds received for the previously announced gold prepay and silver purchase and sale agreements totaling $75 million

- Increased the size of the Granite Creek property package by approximately 1,280 acres (518 hectares), extending exposure along the primary fault structure by approximately 1.6 km north towards the Turquoise Ridge Mine, and 1.6 km south of Granite Creek

- Commenced development of exploration ramp at McCoy-Cove (approximately 1,900 feet of advance now completed); drilling expected to commence in Q4

- Entered into agreement to acquire key water rights for the development of the Cove Project

- Completed first gold sale in Company history

- A total of 208,329 feet (core and RC) drilled by the end of the third quarter

“In the third Quarter the Company achieved record gold sales, more than doubling previous quarter sales .”, stated Ryan Snow, Chief Financial Officer of i-80. “The Residual leaching at both Lone Tree and Ruby Hill has gone well and increases in production and sales were recorded during the quarter. We continued to invest in exploration generating tremendous results and new discoveries at both Granite Creek and Ruby Hill. In addition, we continue to advance the engineering study at Lone Tree on plan and we completed a scoping study on restarting the oxide mill at Ruby Hill.”

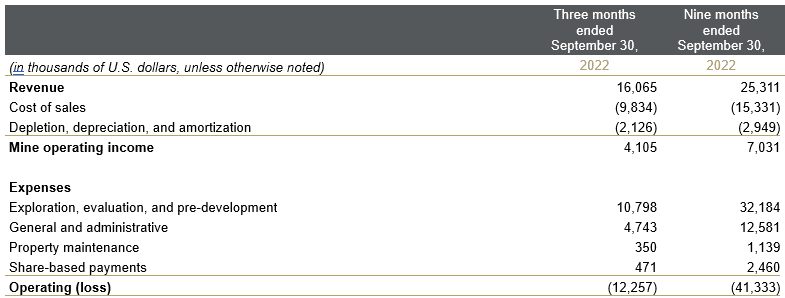

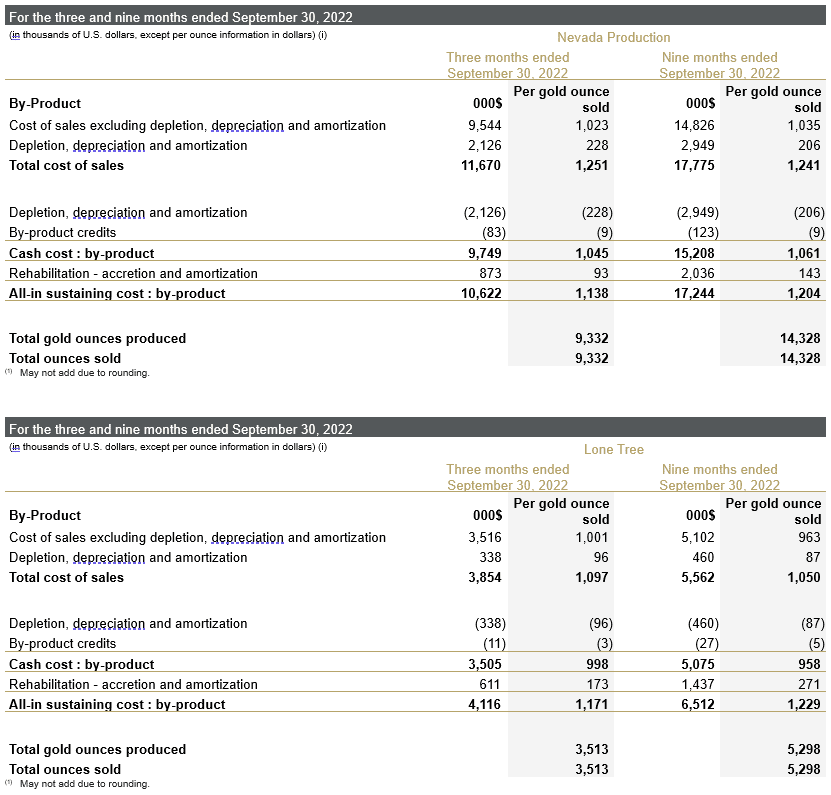

Production and sales from residual leaching at Ruby Hill and Lone Tree totaled 9,332 ounces for the quarter and 14,328 ounces year to date at cash costs per ounce sold of $1,045 and $1,061, respectively, and all-in sustaining cost per ounce sold of $1,138 and $1,204, respectively.

Exploration, evaluation, and pre-development costs were $10.8 million in Q3 and $32.2 million year to date (YTD). This spend reflects mainly the exploration and pre-development work at Granite Creek and Ruby Hill.

Lone Tree Processing Facilities

Lone Tree is expected to become the hub of i-80’s Nevada operations and the central processing facility for mineralization from the first four planned mining projects. Importantly, Lone Tree is host to infrastructure that, following successful refurbishment efforts, will position i-80 as one of only three companies in the United States capable of processing both oxide and refractory mineralization.

During the quarter, the Company continued to advance the detailed engineering study for the restart of the autoclave. The study is progressing on plan and is expected to be completed in the fourth quarter of 2022. Permitting work on Buffalo Mountain continued during the quarter and a drill program was started.

Residual leaching activities at Lone Tree produced 3,513 ounces gold during Q3 and 5,298 YTD at a cash cost per ounce sold of $9981 and $9581, respectively, and all-in sustaining cost per ounce sold of $1,1711 and $1,2291, respectively.

Granite Creek

In the third quarter, 2022, drilling continued for resource expansion on the Ogee and South Pacific Zones with multiple high-grade intercepts. Completed 10,526 feet of core drilling and 5,460 feet of RC drilling during the quarter. The amount of drilling completed as of September 30, 2022 totaling 83,887 feet was in line with the Company’s drilling plan. Drilling targets were expansion and delineation of the newly discovered South Pacific Zone as well as delineation drilling that targeted the Otto, Adam Peak, Range Front and Ogee fault zones with underground drilling.

McCoy-Cove

Total development through the end of the third quarter was 1,938 feet including 1,735 feet for construction of the exploration ramp which continued on plan. Additional work on metallurgical and hydrology studies, engineering of de-watering and mining options, and reclamation activities associated with the inactive tailings storage facility is also being advanced. It is expected that the underground drill campaign will commence in Q4 2022.

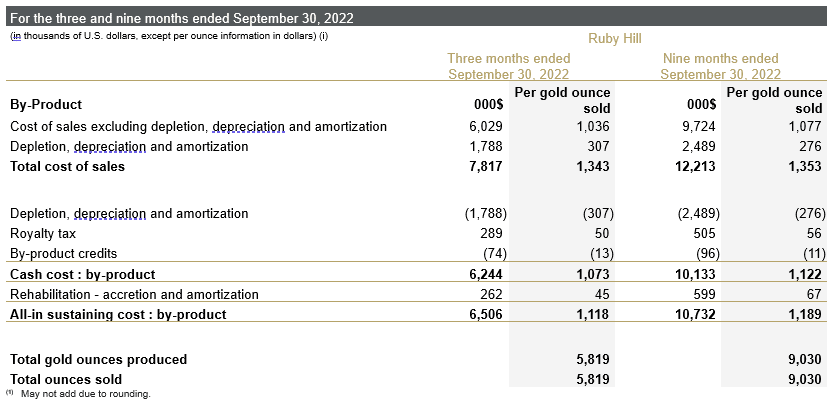

Ruby Hill

In the third quarter, infill and step-out drilling of the Ruby Deeps, 426 and Hilltop zones continued with multiple high-grade intercepts and multiple brownfield exploration targets tested. 17,025 feet of core drilling and 34,865 feet of RC drilling was completed during the quarter, with a combined total of 120,692 feet completed in the first nine months, in line with the Company’s drilling plan. Owing to the substantial success of the 2022 exploration campaign at Ruby Hill, the program has been expanded.

The Company continued to advance permitting for the construction of a decline to access the high-grade Ruby Deeps deposit and the Blackjack Zone with the intent of trucking refractory mineralization for processing at Lone Tree. The Company also completed a scoping study during the quarter for the restart of the existing oxide mill

Residual leaching activities at Ruby Hill produced 5,819 ounces gold during Q3 and 9,030 YTD at a cash cost per ounce sold of $1,0731 and $1,1221, respectively, and all-in sustaining cost per ounce sold of $1,1181 and $1,1891, respectively.

| Conference Call Participant Details | |

| Webcast URL: | https://app.webinar.net/XGDgY2P3lMp |

| Confirmation #: | 5905476 |

| Phone Number Information: | North American Toll-free: 1-888-882-4478 |

Qualified Person

The scientific and technical information contained in this press release was reviewed by Tim George, PE, Mining Operations Manager, and a Qualified Person within the meaning of National Instrument 43-101.

About i-80 Gold Corp.

i-80 Gold Corp. is a well-financed, Nevada-focused, mining company with a goal of achieving mid-tier gold producer status through the development of multiple deposits within the Company’s advanced-stage property portfolio anticipated to be processed at the centrally located Lone Tree processing facility and autoclave.

For further information, please contact:

Ewan Downie – CEO

Ryan Snow – CFO

Matthew Gollat – EVP Business & Corporate Development

info@i80gold.com

Forward-looking information

Certain statements in this release constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws, including but not limited to, actual production results and costs, results of operation outcomes and timing of updated technical studies at the Company’s mineral projects, timing to advance mineral projects to production and advance permitting and feasibility work on the on its mineral projects and future production, development and exploration results. Such statements and information involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the company, its projects, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as “may”, “would”, “could”, “will”, “intend”, “expect”, “believe”, “plan”, “anticipate”, “estimate”, “scheduled”, “forecast”, “predict” and other similar terminology, or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. These statements reflect the Company’s current expectations regarding future events, performance and results and speak only as of the date of this release.

Forward-looking statements and information involve significant risks and uncertainties, should not be read as guarantees of future performance or results and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements or information, including, but not limited to: material adverse changes, unexpected changes in laws, rules or regulations, or their enforcement by applicable authorities; the failure of parties to contracts with the company to perform as agreed; social or labor unrest; changes in commodity prices; and the failure of exploration programs or studies to deliver anticipated results or results that would justify and support continued exploration, studies, development or operations. For a more detailed discussion of such risks and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, refer to i-80’s filings with Canadian securities regulators, including the most recent Annual Information Form, available on SEDAR at www.sedar.com.

NON-IFRS FINANCIAL PERFORMANCE MEASURES

The Company has included certain terms or performance measures commonly used in the mining industry that are not defined under IFRS in this document. These include: by-product cash cost per ounce sold, by-product all-in sustaining cost (“AISC”) per ounce sold, earnings before interest, tax, depreciation and amortization, capital expenditures (expansionary), capital expenditures (sustaining), adjusted net earnings and average realized price per ounce. Non-IFRS financial performance measures do not have any standardized meaning prescribed under IFRS, and therefore, they may not be comparable to similar measures employed by other companies. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS and should be read in conjunction with the Company’s Financial Statements.

Definitions

Adjusted earnings / (loss) and adjusted earnings / (loss) per share excludes significant write-down adjustments and the gain / (loss) from financing instruments.

All-in sustaining costs on a by-product basis per ounce include total production cash costs on a by-product basis and costs related to sustaining production.

Average realized gold price represents the sales price of gold per ounce before deducting mining royalties, treatment and refining charges and gains or losses derived from the offtake agreement with Orion.

By-product credits include revenues from the sale of by-products from operating mines.

Capital expenditure (expansionary) is a capital expenditure intended to expand the business or operations by increasing production capacity beyond current levels of performance and includes capitalized exploration.

Capital expenditure (sustaining) is a capital expenditure necessary to maintain existing levels of production. The sustaining capital expenditures maintain the existing mine fleet, mill and other facilities so that they function at levels consistent from year to year.

Cost of sales per ounce sold is calculated by dividing the attributable cost of sales by the attributable ounces sold.

Exploration and evaluation (sustaining) expense is presented as mine site sustaining if it supports current mine operations.

Rehabilitation – accretion and amortization include depreciation on the assets related to the rehabilitation provision of gold operations and accretion on the rehabilitation provision of gold operations.

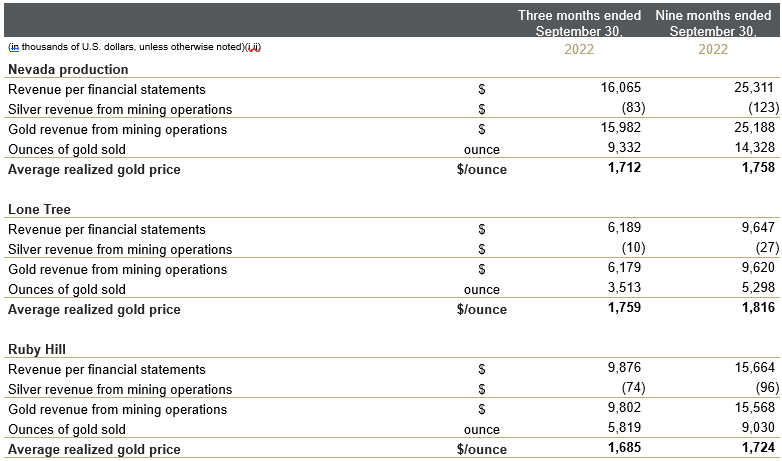

Average realized gold price per ounce of gold sold

Average realized gold price per ounce of gold sold is a non-IFRS measure and does not constitute a measure recognized by IFRS and does not have a standardized meaning defined by IFRS. It may not be comparable to information in other gold producers’ reports and filings.

(i) May not add due to rounding.

(ii) Revenue from 2021 was related to the Company’s 40% interest in the South Arturo mine. On October 14, 2021, the Company completed the asset exchange with NGM and South Arturo was classified as a discontinued operation. Revenue from 2022 relates to the residual heap leaching operations continuing at Lone Tree and Ruby Hill.

Cash Costs

Cash costs per ounce sold represents all direct and indirect operating costs related to the physical activities of producing gold, including on-site mining costs, processing, third-party smelting, refining and transportation costs, on-site general and administrative costs, community site relations, royalties and royalty taxes. State of Nevada net proceeds taxes are excluded. Cash costs incorporate the Company’s share of production costs but exclude, among other items, the impact of depletion, depreciation and amortization (“DD&A”), reclamation costs, financing costs, capital development and exploration and income taxes. In order to arrive at consolidated cash costs, the Company includes its attributable share of total cash costs from operations where less than 100% interest in the economic share of production is held.

Cash cost: by-product – When deriving the cash costs associated with an ounce of gold, the Company includes by-product credits, as the Company considers that the cost to produce the gold is reduced as a result of the by-product sales incidental to the gold production process. Accordingly, total production costs are reduced for revenues earned from silver sales.

Cash costs per ounce is a common financial performance measure in the mining industry, but the term does not have any standardized meaning. In determining its cash cost and cash cost per ounce, the Company has considered the guidelines provided by the World Gold Council, a non-regulatory, non-profit market development organization for the gold industry. A Company’s adoption of the standard is voluntary and other companies may quantify these measures differently as a result of different underlying principles and policies applied.

All-in Sustaining Costs (“AISC”)

AISC include total production cash costs incurred at the Company’s mining operations, which forms the basis of the Company’s by-product cash costs. Additionally, the Company includes sustaining capital expenditures which are expended to maintain existing levels of production (to which costs do not contribute to a material increase in annual gold ounce production over the next 12 months), rehabilitation accretion and amortization, and exploration and evaluation expenses. The Company does not allocate corporate general and administrative expenses. The measure seeks to reflect the full cost of production from current operations, therefore expansionary capital is excluded. Certain other cash expenditures, including tax payments (including the State of Nevada net proceeds tax), dividends and financing costs are also excluded. The Company reports AISC on a per ounce sold basis.

This financial performance measure was adopted as a result of an initiative undertaken within the gold mining industry; however, this performance measure has no standardized meaning and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. In determining AISC, the Company has considered the guidelines provided by the World Gold Council, a non-regulatory, non-profit market development organization for the gold industry. A Company’s adoption of the standard is voluntary and other companies may quantify these measures differently as a result of different underlying principles and policies applied.

The following table provides a reconciliation on a by-product basis for gold cash cost and AISC for the three and nine months ended September 30, 2022:

Adjusted Earnings / (Loss)

Adjusted earnings / (loss) and adjusted earnings / (loss) per share are non-IFRS measures that the Company considers to better reflect normalized earnings because it eliminates non-recurring items. Certain items that become applicable in a period may be adjusted for, with the Company retroactively presenting comparable periods with an adjustment for such items and conversely, items no longer applicable may be removed from the calculation. Neither adjusted earnings / (loss) nor adjusted earnings / (loss) per share have any standardized meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other companies.

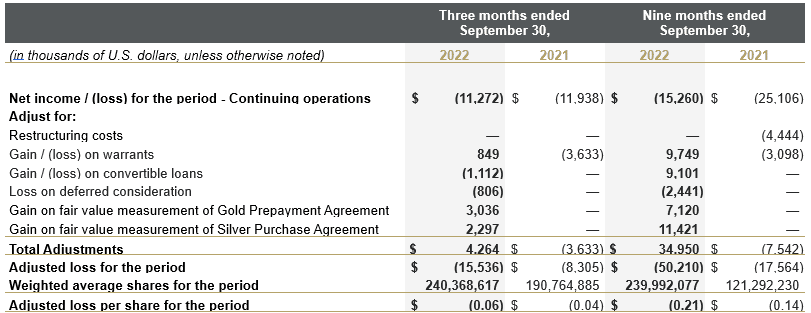

The following table shows a reconciliation of adjusted earnings / (loss) for the three and nine months ended September 30, 2022 and 2021, to the net earnings / (loss) for each period.